What is term life insurance and how does it work?

Term life insurance is designed to offer life cover for a set time period. Our helpful guide covers everything you need to know about term insurance.

What is term life insurance?

Term life insurance is a type of life insurance that covers you for a set period of time. This is known as the ‘term’. You can choose how long you want your cover to last. Anything from five to 50 years. It’s different to whole of life insurance because it has an end date. Whole of life insurance stays in place for your whole life and pays out whenever you die.

Many people take out term insurance to cover the time they’re paying back a mortgage, say 30 years. Or when their children are still dependent on them. If you pass away or are diagnosed with a terminal illness during that time, the policy pays out a lump sum. This payout can be used to cover financial commitments such as:

• mortgage and rent payments

• household bills and day to day expenses

• childcare or education costs.

It’s designed to provide financial support for your loved ones during the time when they need it most.

How does term life insurance work?

1. Choosing your cover

When you apply for term life insurance you’ll need to have an idea about:

• who you want to cover

• how long you want the policy to last

• how much cover you’ll need

• whether you want increasing, decreasing or level cover.

You can use these details to get a quote which will show you how much your insurance will cost.

2. Applying for cover

During the application you’ll need to give the insurer your personal details. And provide information about your health and lifestyle. You may also be asked about any existing life insurance you have and whether you’ve had life insurance declined. The final cost of your cover depends on the answers to these questions.

This process needn’t take long, unless you have a complicated medical history. But you must be open and honest about your health. If you don't fully disclose all your medical details, it can cause problems when a claim is made.

Some insurers, like Vitality, will provide free ‘immediate cover’ while your application is in the assessment or underwriting process, provided eligibility criteria are met. This means if you die unexpectedly, your loved ones may receive a payout.

With Vitality, the ‘immediate cover’ amount equals the Life Cover amount you applied for, capped at £500,000. It is only available on new plans and only covers death – it does not pay out for terminal illness.

3. Paying premiums

Premiums are usually paid monthly by direct debit. To stay insured you need to keep paying the premiums throughout the term of the policy. If you stop, the cover may lapse.

4. Making a claim

When you die your beneficiaries need to tell the insurance company and provide some details about your policy. The claim will be assessed and other documentation, like a death certificate, may be needed. Only when the claim is approved does the payout take place.

Claims are subject to assessment, policy terms and exclusions, and may be declined.

How much term life insurance do I need?

Everyone’s needs are different, but as a starting point, take into consideration the following factors:

Expenses

- Outstanding debts. These can include your mortgage, personal loans, car loans and credit cards.

- Current living expenses. Such as childcare, domestic bills, food and entertainment. Multiply the annual cost by how long your dependents will need financial support for.

- Future expenses. Like private schooling or further education.

- Funeral costs. The average total funeral spend in the UK is around £5,1401, though costs can be higher or lower depending on individual choices and circumstances.

Revenue

- Existing savings and investments.

- Partner’s income.

- Death in service payments.

Add together all the costs above and subtract any savings, income and other insurances that could contribute to paying for them. This should leave you with the amount of life cover you need.

If you’re not looking for a precise figure, you could choose a multiple of your salary as cover. Death in service payments are often based on four times your current salary.

What are the different types of term life insurance?

There are three basic types of term life insurance. And each one is designed to meet a different need. You can choose to take out more than one type of policy to cover all your insurance requirements.

Level term insurance

Level term life insurance pays out the same fixed sum throughout the term of the policy. You choose the amount when you set up the plan. And the cost of your cover will stay the same as well. So, you know exactly how much it costs each month and how much your family can expect if you die.

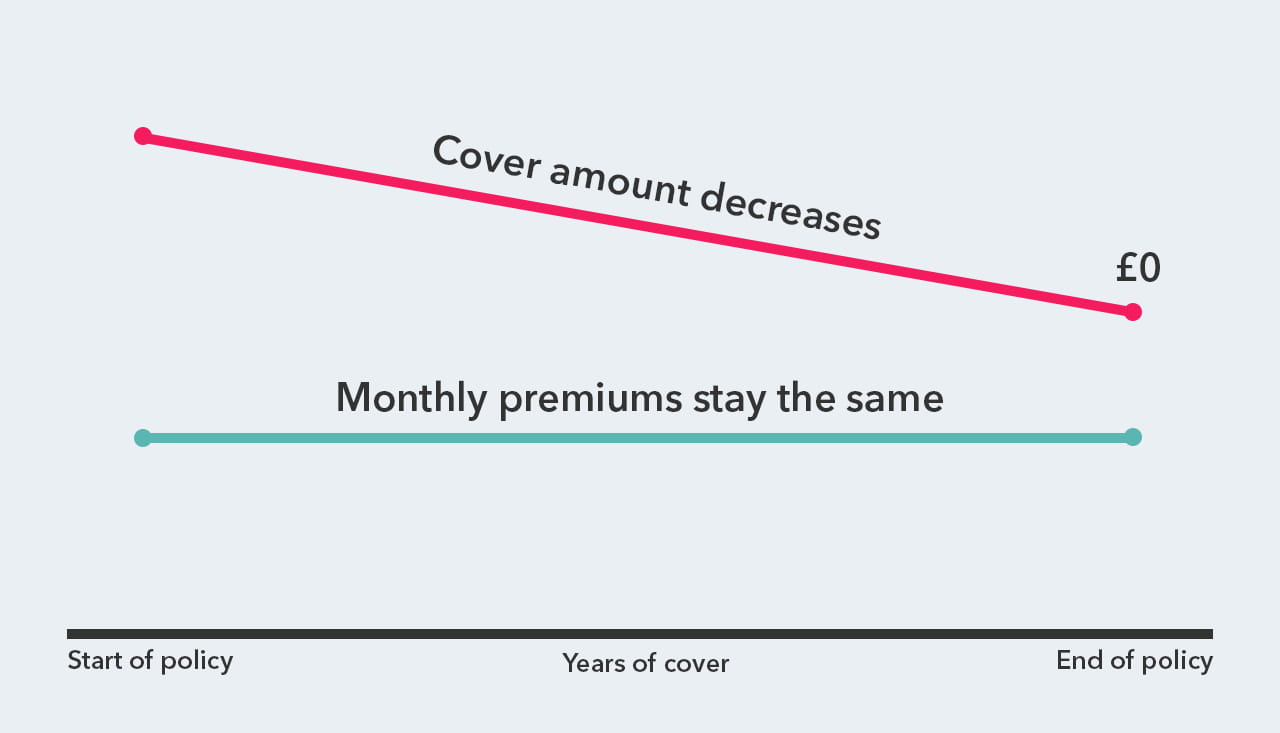

Decreasing term life insurance

With decreasing term life insurance, the payout reduces over time. It’s usually taken out to cover the cost of paying back a repayment mortgage or other debts that decrease each year. Your premiums will stay the same throughout the term of the policy. And it can be a cheaper option than level or increasing term insurance as the payout diminishes over time.

Increasing term insurance

This type of insurance provides a payout that increases over time. It’s usually set up to keep pace with inflation or rising financial obligations. As the payout increases over time, so will your premiums.

Here's how the insurances compare:

| Level term life insurance | Increasing term life insurance | Decreasing term life insurance | |

|---|---|---|---|

| Payout on death |

Stays the same. | Increases each year. | Reduces each year. |

| Premiums |

Stay the same throughout the term of the plan. | Monthly payments increase as the cover increases. | Stay the same throughout the term of the plan. |

| Suitable for |

Debts that don’t increase, like an interest only mortgage. | Day to day expenses that increase as the cost-of-living rises. | Debts that reduce over time, like a repayment mortgage. |

| Cover | Should provide enough cover throughout the plan as long as the debt doesn’t increase. | Cover keeps its real value over time. Protects your family’s future needs. | Important to check that the decreasing cover still meets your needs each year. |

How do term life insurance quotes and rates work?

If you get quotes from several different providers, you may find that the cost of the cover varies from one to another. This is because each provider assesses risk slightly differently.

Insurance companies will ask you a range of questions about your health and lifestyle and the type of cover you want. They use this information to work out how much to charge you for cover. So, two people may pay different amounts for similar cover just because one is younger than the other.

What affects term life insurance rates?

There are two main factors that affect insurance rates and therefore the premium you’ll pay.

Personal factors. Such as your age, medical history, smoking status and occupation. The younger you are when you start your policy, the cheaper the premiums.

Cover options. Whether you choose level term insurance, increasing or decreasing insurance will affect how much you pay. As will the length of your policy and how much cover you need. And if you take out additional cover, such as serious illness or income protection insurance, this will also affect your premium

Who is term life insurance for?

Term life insurance can be a valuable financial safety net for all stages of life. From buying your first home to starting a family and even leaving a legacy. The options available mean that you can provide financial stability for your loved ones throughout your life.

Term life insurance for families

If your family suddenly lost your income, they may struggle to cope financially. Term life insurance can help pay for household bills, childcare, education fees and holidays. It’s valuable cover for when children are financially dependent on you. It can also take the strain away from the surviving partner to rush back to work following a bereavement.

Term life insurance for mortgages (decreasing cover)

A mortgage is often the largest debt you’ll have. And relies on regular payments that pay it off over time. If you die, your income is no longer available to offset the cost of your mortgage. But the mortgage still needs to be paid. Decreasing term insurance provides a lump sum that you can use to repay the remainder of your mortgage. Thus, eliminating the worry of meeting the regular payments.

Term life insurance for seniors

If you have debts in later life, it can be a good idea to consider having life insurance to cover them if you die. Unfortunately, your debts don't die with you. And your estate will be expected to pay back what you owe, leaving less to your loved ones. A term life insurance plan can help pay off these debts, cover your funeral expenses and even leave a legacy for your family. As an older person your premiums will be more expensive but could still be very worthwhile.

How to choose the right life insurance policy?

Let’s look at the key questions to ask yourself when you’re considering taking out life insurance.

What is the insurance for?

A life insurance policy can be used for anything. But they’re often taken out to:

- Cover debts such as your mortgage, loans and credit cards bills.

- Replace lost income so your family can maintain their lifestyle.

- Leave money to loved ones.

How much insurance do you need?

You can calculate the amount of cover you need by adding up:

- mortgage debt

- loans and credit costs

- day to day living costs

- future expenses, such as further education

funeral costs.

If you have savings or other insurances, you can offset these against how much cover you’ll need.

How long do you need the insurance?

Providers usually offer cover from 5 to 50 years. Most people take out cover for as long as their debts last. So, if you have a 30-year mortgage, you’d want cover for at least 30 years.

Should your partner get cover too?

It can be difficult for one partner to manage on just their wage if the other dies. Joint life insurance is available and can be easily set up for those with joint finances.

Which type of insurance is best?

You can have more than one type of insurance plan. So, you can tailor your cover to different needs. For example, decreasing term life insurance is suitable for repaying a loan that decreases over time. But, if you want to cover living expenses and future costs, you may want to look at level or increasing term life insurance instead.

Key takeaways

- Term life insurance is a type of life insurance that covers you for a set period of time. This is known as the ‘term’. It pays out a lump sum if you die while the policy is in place.

- This payout can be used to cover financial commitments. Such as mortgage and rent payments, household bills, childcare and day to day expenses.

- The cost of cover varies from one provider to another. Your premiums are based on personal factors such as your age and medical history and the cover options you choose.

- Term life insurance is a valuable financial safety net for all stages of life. From buying your first home to starting a family and even leaving a legacy.

Vitality life insurance

Want to know more about life insurance or thinking about taking out a policy? Here are some of the benefits of taking out life insurance with Vitality:

- A brand you can trust - In 2024, we paid out 98.9% of all Life Cover claims.*

- Get a lower monthly premium upfront when you add Optimiser to your plan. Keep your premiums low when you stay active.

- Access to Vitality partner discounts and rewards.

- Get free no-obligation advice. Our advisers offer expert advice to help you make the right decisions.

You're not alone in choosing Vitality. Over 2 million lives in the UK are now covered by our insurance, and we’re here to support you too.

Ready to take the next step? Getting a quote is simple and takes just a few minutes.

*VitalityLife Claims and Shared Value Report 2025